For generations, cash was king. Today, it’s more like a backup quarterback, or according to a recent Harris Poll, cash is even considered “cringe” by Gen Z.

Consumer payment behavior is evolving rapidly, and small businesses across Wyoming need to keep pace. The way your customers want to pay is changing, and your ability to adapt can directly impact sales, customer experience, and long-term competitiveness.

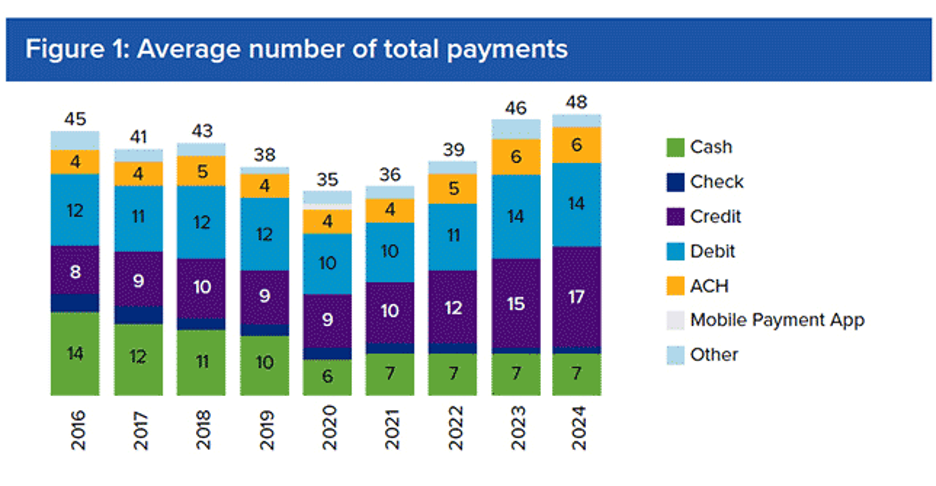

Recent data shows a clear trend: non-cash payments now dominate consumer behavior. Credit cards account for about 35% of transactions and debit cards 30%, while cash has dropped to roughly 14% of payments.

At the same time, consumers are making more total payments per month than ever before, mobile payments are growing fast, and nearly 1 in 4 payments is now remote (online or app-based)

Why Customers Are Choosing Digital Payments

- Convenience - Mobile and card payments are faster, easier, and more flexible. Customers can tap, swipe, or click—often completing transactions in seconds.

- Record Keeping - Digital payments automatically create a transaction history, which helps with budgeting and expense tracking.

- Flexibility - Mobile wallets allow customers to choose between credit, debit, or bank accounts instantly.

- Enhanced Experience - Modern payment systems integrate loyalty programs, discounts, coupons, and digital receipts.

Payment is no longer just a transaction; it’s part of your marketing and customer experience strategy.

Recent Trends

“Tap-to-Pay” is Becoming the Standard - More than half of businesses now use mobile POS systems, allowing payments anywhere. For Wyoming businesses (food trucks, guides, market vendors), this is especially powerful.

Customers Spend More Without Cash -Digital transactions often result in higher average ticket sizes. In some cases, cashless purchases are over 50% higher than cash transactions.

Cash Isn’t Dead, but It’s Changing - Cash still plays a role, preferred by older demographics and lower-income households, used as a backup payment method, and common for small, in-person purchases

The Rise of Peer to Peer and Buy Now Pay Later - Buy Now Pay Later is seeing rapid growth with 15% of Americans having reported using BNPL in 2024, up from 12% in 2022. Over 40% of users now apply it to groceries and daily essentials, not just electronics or apparel. Mobile apps are now used for 50% of person-to-person (P2P) payments

Action Steps for Wyoming Small Businesses

Offer Multiple Payment Options - At a minimum: Credit & debit cards, mobile wallets (Apple Pay, Google Pay), and online payment options.

Upgrade Your POS System - Look for systems that: Accept contactless payments, Integrate with inventory and accounting, and work in mobile environments (key for rural and outdoor businesses)

Leverage Payment Data - Use your system to: Track top-selling items, identify repeat customers, and run targeted promotions

Align With Your Customer Segment - Younger/tourism-heavy markets: prioritize mobile + digital. Local/rural markets: maintain a mix, including cash

Think Beyond the Transaction Consider: Loyalty programs, Digital receipts, and pre-ordering or online booking

The shift away from cash isn’t just about technology, it’s about meeting customer expectations. Small businesses that embrace flexible, modern payment options:

- Reduce friction at checkout

- Increase average sales

- Build stronger customer relationships

If you’re unsure where to start, the Wyoming SBDC is here to help. From selecting the right POS system to aligning your payment strategy with your target market, our advisors can guide you every step of the way.

- - -

The Wyoming SBDC Network is hosted by the University of Wyoming with state funds from the Wyoming Business Council. Funded in part through a Cooperative Agreement with the U.S. Small Business Administration. Full funding disclosures available at

wyomingsbdc.org/about

All opinions, conclusions, and/or recommendations expressed herein are those of the author(s) and do not necessarily reflect the views of the SBA.